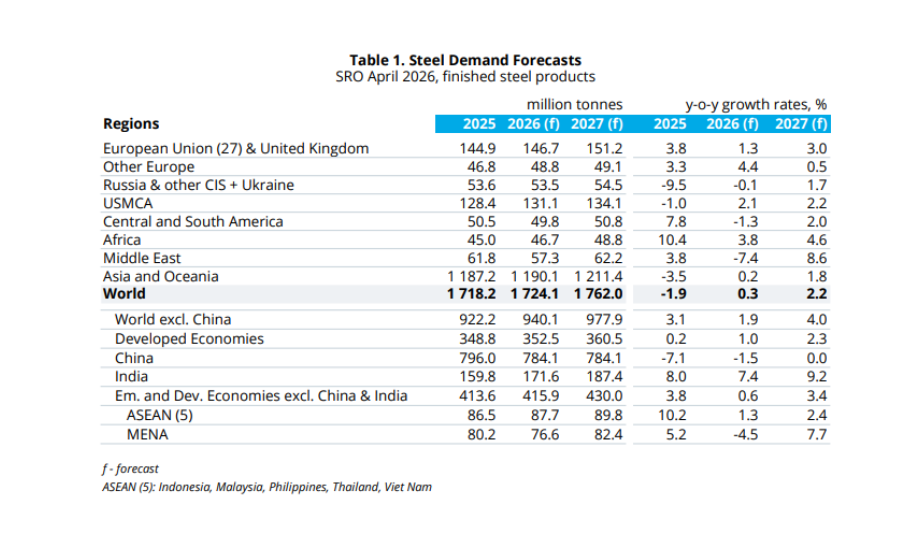

Global Steel Demand Forecast to Grow 0.3% in 2026 and Accelerate to 2.2% in 2027

On April 14, 2026, the World Steel Association released its Short Range Outlook (SRO) report on global steel demand for the 2026–2027 period. According to the report, global steel demand in 2026 is projected to reach approximately 1.724 billion tons, representing a modest 0.3% increase compared to the previous year. In 2027, growth is expected to accelerate to around 2.2%, bringing total demand to approximately 1.762 billion tons.

Source: World Steel Association (WSA)

The global steel market is projected to transition from modest growth in 2026 to a more pronounced recovery trend in 2027, as improving economic conditions vary across regions. In China, the decline in steel demand is expected to slow in 2026, while major developing economies, particularly India, are projected to maintain strong growth momentum. At the same time, geopolitical tensions in the Middle East could weigh on the market, potentially leading to a sharp contraction in regional steel demand in 2026, contrary to earlier expectations of growth. Meanwhile, major developed economies are beginning to recover after a prolonged downturn, with the European Union, the United States, Canada, Japan, and South Korea all forecast to return to positive growth by 2027. Overall, global steel demand excluding China is expected to grow by approximately 4.0% in 2027, marking a relatively strong performance compared with recent years.

These forecasts are based on data updated through mid-March 2026, assuming that the conflict in the Middle East will conclude by June of the same year. Under this scenario, most major economies are considered resilient. The United States, China, and India are expected to face limited direct spillover impacts, while the European Union—despite its significant energy dependence—has strengthened its adaptability following the Russia–Ukraine war energy crisis in 2022. However, if the conflict extends beyond the second quarter of 2026, the outlook would likely require substantial downward revisions, particularly for regions heavily reliant on energy supplies.

Source: World Steel Association (WSA)

China: Moving Toward Cyclical Stabilization

In 2026, China’s steel demand is projected to decline by approximately 1.5% compared with 2025. The contraction is expected to narrow as the real estate market gradually reaches its bottom, infrastructure investment sees modest growth supported by local government measures, and manufacturing demand continues to expand moderately, driven by stronger export activity.

By 2027, steel demand is forecast to remain broadly stable compared with 2026, as the restructuring of the real estate sector is largely completed. This transition is expected to help the market move into a more stable phase following the prolonged downturn that began in 2021.

Developing Economies (Excluding China)

Steel demand growth in developing economies is expected to slow to 2.5% in 2026, mainly due to a sharp downturn in the Middle East and the normalization of demand in ASEAN following a period of inventory restocking. However, growth is projected to rebound to 5.1% in 2027, supported by stronger momentum in developing Asia, Africa, and improving market conditions in the Middle East.

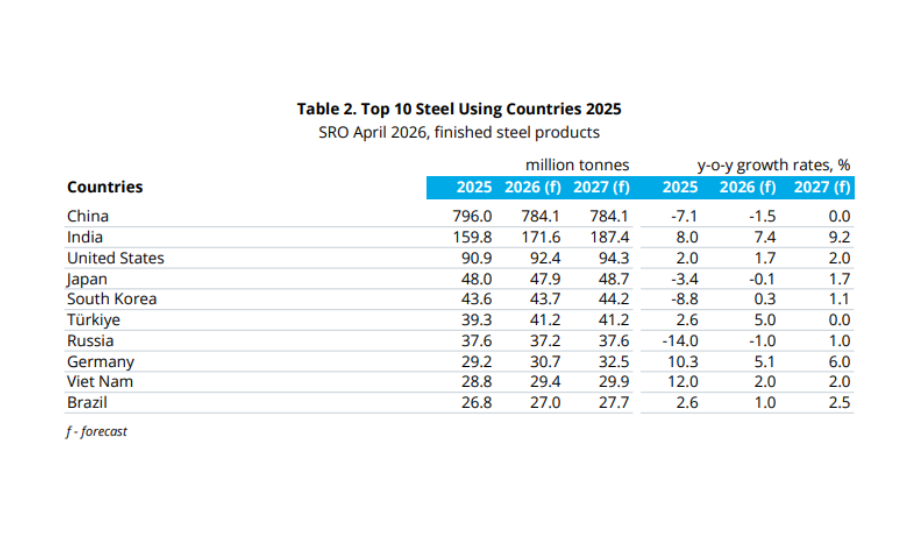

India: A Leading Growth Driver

India continues to lead global growth, with steel demand projected to increase by 7.4% in 2026 and 9.2% in 2027. The primary drivers include large-scale infrastructure investment, strong expansion in the automotive sector, railway network development, and rising demand for durable consumer goods supported by improving income levels.

Africa

The region has maintained a clear recovery momentum since 2023, with steel demand growth forecast at 3.8% in 2026 and 4.6% in 2027. This trend reflects rapid urbanization, increasing infrastructure investment, and ongoing economic diversification, positioning Africa as an important growth engine for the global steel market.

Developed Economies

After a modest 0.2% increase in 2025, steel demand in developed economies is projected to gradually recover, growing by 1.0% in 2026 and 2.3% in 2027, although remaining significantly below pre-crisis levels.

- European Union and the United Kingdom: Demand is expected to grow by 1.3% in 2026 and 3.0% in 2027, supported by infrastructure and defense investment as well as improving household income, while continuing to face risks from high energy prices.

- United States: Steel demand is forecast to increase by 1.7% in 2026 and 2.0% in 2027, driven by technology investment, infrastructure development, and a recovery in residential construction, though constrained by high interest rates, elevated material costs, and labor shortages.

In summary, the global steel market outlook for 2026–2027 indicates a clear transition from the “bottoming-out” phase in 2025 to a period of recovery during 2026–2027, despite the significant escalation of global trade tensions and ongoing geopolitical uncertainties. This positive outlook is supported by the proven resilience of the global economy, sustained strength in public infrastructure investment across most major economies worldwide, and expectations of gradually easing financial conditions.

However, the road ahead is not without challenges, as:

- First, the global manufacturing sector continues to face pressure from rising production costs and weakening consumer affordability.

- Second, escalating trade tensions are having a direct and negative impact on steel demand in economies heavily reliant on exports of steel-intensive goods, such as machinery and automotive components.

- Finally, geopolitical uncertainties remain a major constraint, dampening both consumer and investor confidence while restraining steel demand across key markets.

Source: Report by the World Steel Association (April 14, 2026)

Các tin khác

-

Phone:(+84 273) 364 2555

-

Fax:(+84 273) 364 2557

-

Email:info@vinlonginox.com

sales@vinlonginox.com

sales@vinlonginox.vn

CÔNG TY TNHH THÉP KHÔNG GỈ QUẢNG THƯỢNG VIỆT NAM

VINLONG STAINLESS STEEL (VIETNAM) CO., LTD.

TAX ID: 1201462743